The Future Automated American Economy

Steam gave us modern economic growth. Robotics will drive the next wave of human prosperity.

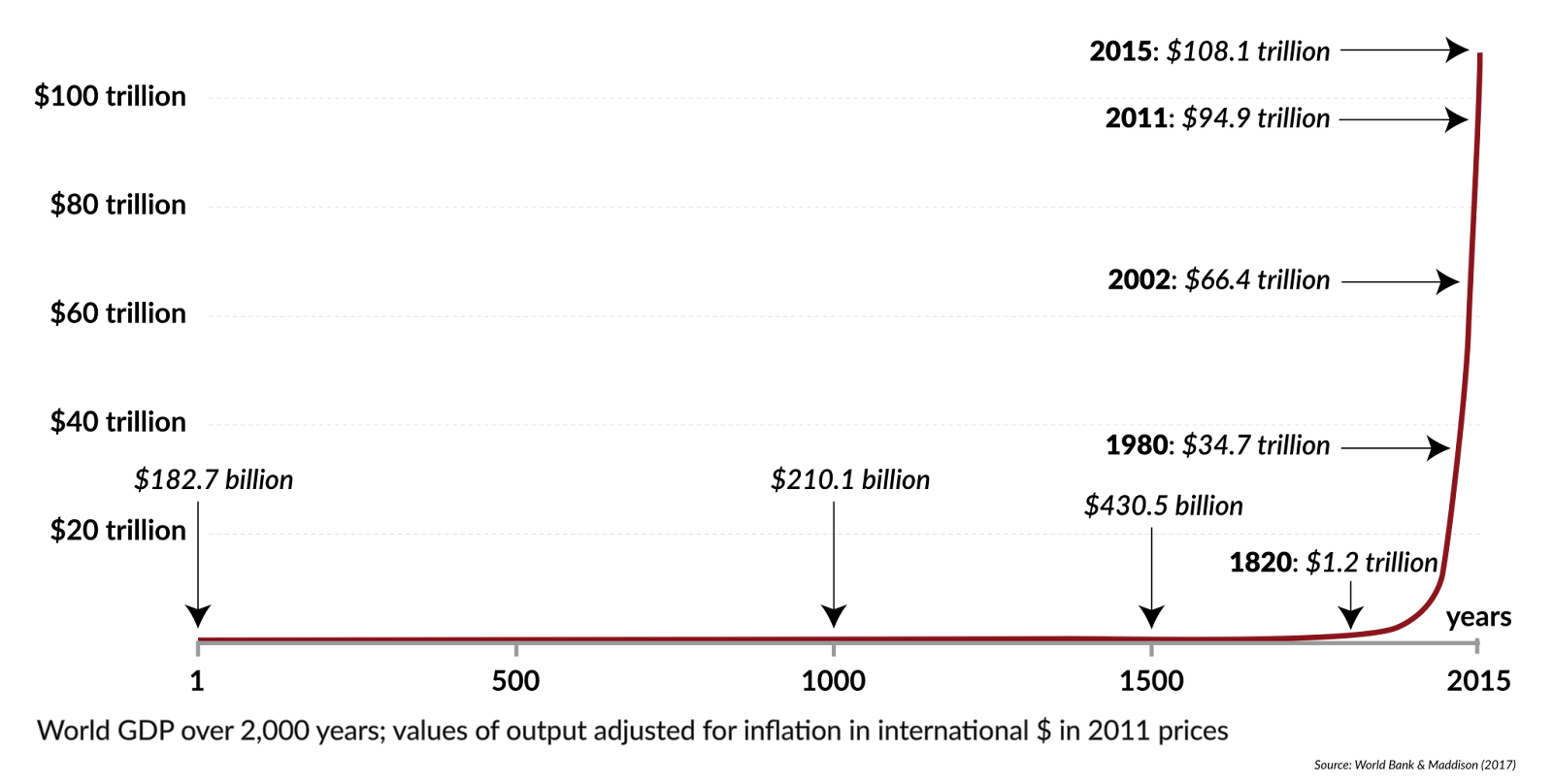

Most of human history has been defined by grinding poverty.

Our hunter-gatherer ancestors experienced functionally zero economic growth — life was simply a matter of survival, dependent on nomadically tethering oneself to the movement of wild animal herds. Then, about 10,000 years ago, we figured out the basics of agriculture and, later, animal husbandry, which allowed humanity to begin eking out the barest subsistence. This created some amount of consistency and certainty in daily life, which then required developing institutions and systems for managing time-spatial relationships. The result was the emergence of more complex social arrangements, like religion and government.

But after the Agricultural Revolution, growth stalled again and humanity settled into thousands of years of more marginal improvements in economic growth.

Source: GIS Reports

Economic growth in the pre-Industrial era averaged roughly 0.1 percent per year — essentially, stagnation was the norm for most of human history. Once James Watts’ steam engine entered onto the world stage — around 1760 — that number probably quadrupled or quintupled to 0.4-0.5 percent for the next few decades. By unshackling economic growth from the constraints imposed by the upper bound limits of human and animal energy expenditures, the Industrial Revolution gave birth to an entirely new economic reality. By the modern era, 2-3 percent growth has come to represent normal expectations.

Now, in a world of advanced AI, some throw out pretty wild annualized growth projections of what the future heralds — 5, 10, even 20 percent!

But it seems hard to imagine a world in which the AI we’re all using today somehow manages to quadruple current growth numbers. Sure, ChatGPT is a great advancement in the evolution of search, but it’s not clear how you get from that to immensely higher productivity in, say, manufacturing. This has become an increasing fixture of recent AI conversations — that the new models and systems, while good, aren’t exactly heralding the promised revolution of a post-scarcity society – and many companies, more so than individuals, seem to be having a difficult time making sense of how to leverage this new technology effectively.

As I noted in my initial post, the lack of a clear vision for AI applications and use-cases will inevitably hold back the fullest promise of this technology’s potential. That’s one of the many reasons I’m so bullish on robotics. Robotics and automation offer that compelling vision — one that can easily make up the difference between current economic growth figures and projected growth.

Much is being made about forecasts for the total addressable market (TAM) for AI, with estimates running a pretty wide gamut, from a few hundred billion dollars per year just for direct generative AI to nearly $15 trillion, which accounts for the indirect benefits to productivity improvement and increased consumer demand. Any way you slice that range, it’s a lot of money. But the possible TAM for the entire range of robotics, from industrial applications to humanoid variants, could, by at least one estimate, run in the tens of trillions of dollars.

If you imagine a future where robots move from a backend curiosity largely confined to warehouses and assembly lines to a more ubiquitous feature of everyday life, then that number isn’t beyond the realm of possibility. That future isn’t too tough to imagine, especially in a world where one needs to strain to see anything but diminishing marginal returns in digital sectors (after all, advertising optimization can only do the heavy lifting of adding to GDP for so long).

In short, the future low-hanging fruit in productivity gains will almost certainly be found in the physical realm, for three reasons:

The decreasing marginal cost curve of robotics;

The historic long-tail value of automation; and

The inability of human labour to scale effectively in industries that need more workers.

One way to think about robotics is through the lens of cost curves. For decades, actuators, sensors, and semiconductors made robots too expensive for broad deployment outside of highly specialized settings like automotive assembly lines. But that bill is now falling by double digits annually, and the average selling price of humanoid robots is expected to follow suit. This looks a lot like the early trajectory of solar panels or lithium-ion batteries: once the learning effects kick in and production scales, the marginal cost of each additional unit drops fast. At that point, the economics shift from “expensive experiment” to “why wouldn’t you automate this?”

Still, robotics isn’t just another consumer electronics story. Rather, it’s a continuation of the story that has defined the modern economic growth miracle: automation. The development of the steam engine heralded the Industrial Revolution, but that process has only accelerated since the 18th century. From the cotton gin to the train, the last two hundred years of human history has primarily been a story of freeing human labour from the toils of the fields to be directed towards more creative and intellectual pursuits, which in turn has yielded the scientific and technological breakthroughs that have made further advancements and refinements to automation possible. AI and robots are just the latest chapter in this tale. The value of automation, like other technological advancements, compounds over time, and will almost certainly continue to compound long into the future.

Economists like Daron Acemoglu and Pascual Restrepo have emphasized that robots are what they call “automation capital”: they don’t just complement labour like computers do, they often substitute directly for human tasks. That’s why the productivity gains from robots can be enormous — McKinsey estimates automation could add up to $4.5 trillion to global GDP annually by 2030 — but the distributional effects are messy. Some jobs disappear, others are reconfigured, and entirely new roles spring up around maintenance, programming, and system integration. The 20th-century story of mechanization in agriculture, where labour productivity skyrocketed while total employment in the sector plummeted, is an instructive parallel.

At the same time, the “robots will take all the jobs” narrative misses something important. The bigger problem isn’t too much automation, but too little. We’re still in a world where healthcare assistants spend hours on paperwork, logistics firms struggle with chronic labour shortages, and infrastructure projects are constrained by workforce bottlenecks. One of the fundamental problems affecting these sectors is Baumol’s “cost disease,” where labour-intensive industries tend to be more immune to the technology-driven productivity improvements in other sectors. Healthcare, education, and elder care get more expensive over time because they rely on human labour that doesn’t scale. Robotics has the potential to break that dynamic by introducing productivity growth into precisely those stagnant sectors. If humanoid robots can reliably lift patients, monitor vital signs, or handle routine logistics, the economic ripple effects are transformative.

Of course, none of this plays out in a vacuum. The global competition for robotics leadership is already intense. China currently dominates many of the hardware components (e.g, motors, rare earth magnets, actuators) while the US leads in AI software and chip design. This asymmetry matters. Even as the US maintains its dominance in this technology’s “brain” the “body” of robotics is heavily dominated by non-US firms. History shows that countries which lead in the physical manufacturing layer often set the pace for adoption and standardization. If the US wants to avoid being caught flat-footed, it needs to treat robotics as both an economic and strategic priority.

So what should policy do?

To begin, as I noted in a previous post, the US needs a National Robotics Strategy, if only to create a clear vision for coordinating policy questions related to accelerating the development and adoption of robotics, and the industry more generally. Such a strategy should, however, delve deeper into a number of issues of national importance.

Data escrow and sharing frameworks. For advanced robotics to flourish, developers need access to vast amounts of real-world interaction data. Yet competitive pressures, high costs of generation, and liability concerns often keep this data siloed. A national data escrow system would give firms incentives to contribute without fear of losing proprietary edge. By pooling diverse datasets, the US can accelerate training, improve safety, and ensure robots can navigate the unpredictable messiness of human environments. Without such mechanisms, progress risks being bottlenecked by fragmented datasets and mistrust, leaving the US at a disadvantage in the global robotics race.

Lower the barriers to adoption. Just as renewable energy took off once tax credits and accelerated depreciation made projects pencil out, robotics could benefit from similar tools. Small and medium-sized manufacturers — the firms least able to absorb upfront capital costs — should be able to claim credits for investing in robotics systems. Public procurement can also play a role. If the government becomes an early adopter, piloting robots in infrastructure, defense logistics, or elder care facilities, it both creates scale and signals legitimacy.

Invest heavily in the fundamentals. Robotics isn’t only about AI models; it’s about reliable sensors, lightweight materials, efficient batteries, and robust manufacturing processes. Federal R&D funding should target these “unsexy” components, because they are where supply chains are fragile and where global competitors have an edge. Think of it as the CHIPS Act for actuators and power systems.

Don’t neglect the workforce. History is clear that automation without adaptation breeds backlash. Reskilling programs, community college curricula, and apprenticeships focused on robotics maintenance and programming should be front-loaded into any national strategy. The key is not to prevent automation but to make sure its benefits are broadly shared.

Standards and safety frameworks. If robots are going to operate in warehouses, hospitals, and public spaces, interoperability, cybersecurity, and physical safety cannot be left to voluntary compliance. The US will need to harmonize rules so companies aren’t navigating a patchwork of liability regimes. Without trust, adoption stalls; and without adoption, the productivity gains never materialize.

The economic logic of robotics points toward acceleration: falling costs, rising demand, global competition. The policy logic points toward urgency: build institutions, create incentives, fund the basics, support workers, and standardize safety. The upside is enormous. We could be looking at the biggest infusion of productivity growth since electrification. But history also shows that general-purpose technologies don’t diffuse automatically. They spread because societies built the institutions to guide them — from railroads to the Internet.

Robotics deserves the same treatment. The stakes aren’t just industrial efficiency, but who captures the next wave of global economic leadership. If the US wants to lead in the era of embodied AI, the time to act is now.